Business

Oil Prices Plummet Amid Trump Tariff Announcement Concerns

NEW YORK, April 2 (Reuters) – Oil prices fell into negative territory on Wednesday following a surge of a dollar in post-settlement trading as U.S. President Donald Trump announced tariffs on international trading partners, raising fears of a global trade war that could reduce demand for crude oil.

Brent crude futures closed 46 cents higher, or 0.6%, at $74.95 a barrel, while U.S. West Texas Intermediate (WTI) crude futures rose by 51 cents, or 0.7%, to settle at $71.71. Following Trump’s press conference, U.S. futures saw a dollar increase before turning negative, amid apprehensions regarding his stated tariff plans.

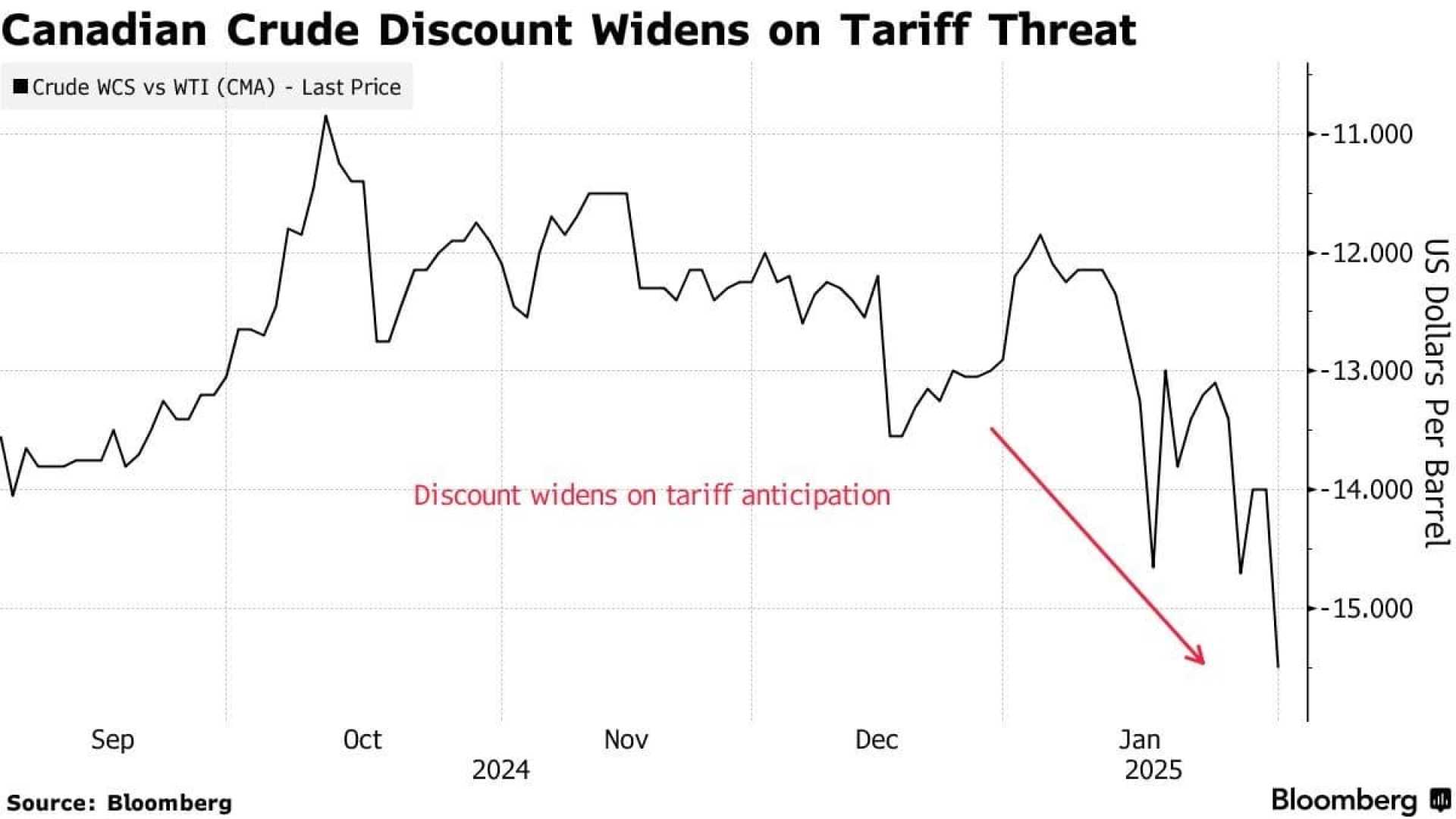

For weeks, Trump had advertised April 2 as a pivotal ‘Liberation Day’, indicating new duties that could alter the global trade landscape significantly. Notably, a chart presented by Trump during the conference omitted details about tariffs on Canada and Mexico, key players as Canada exports approximately 4 million barrels of oil per day to the United States.

Experts predict that Trump’s tariff policies could lead to inflation, reduced economic growth, and heightened trade tensions, factors that are currently constraining oil price escalation. “Crude prices have paused last month’s rally, with Brent meeting resistance above $75, with attention shifting from sanctions on supply to the repercussions of Trump’s tariff announcements,” said Ole Hansen, head of commodity strategy at Saxo Bank.

Comments made by Mexico’s President Claudia Sheinbaum on Wednesday indicated that Mexico does not intend to retaliate with tariffs against the U.S., amidst discussions of potential trade conflicts.

Additionally, Trump voiced threats of imposing tariffs on Russian oil, while reinforcing a toughened stance on Iran as part of his “maximum pressure” campaign to limit Iranian oil exports.

Russia, the world’s second-largest oil exporter, contributed to market volatility on Wednesday by suspending operations on a key oil export route at the Black Sea port of Novorossiisk a day after restricting loadings from an essential Caspian pipeline, affecting Russian output of close to 9 million barrels per day.

Meanwhile, market reaction to U.S. government crude inventory data remained subdued despite reports indicating a surprising build of approximately 6.2 million barrels last week. Giovanni Staunovo, a UBS analyst, remarked, “While the inventory data was bearish, the market perceived it neutrally as it was fueled by a significant rise in Canadian crude imports, likely stemming from concerns over looming tariffs.”

As oil traders brace for the implications of Trump’s tariff declarations, analysts have cautioned against premature conclusions regarding market direction given the uncertainty surrounding the policy’s enforcement and potential global repercussions.