Business

New Tax Bill Introduces Changes Benefiting Salaried Employees and Property Buyers

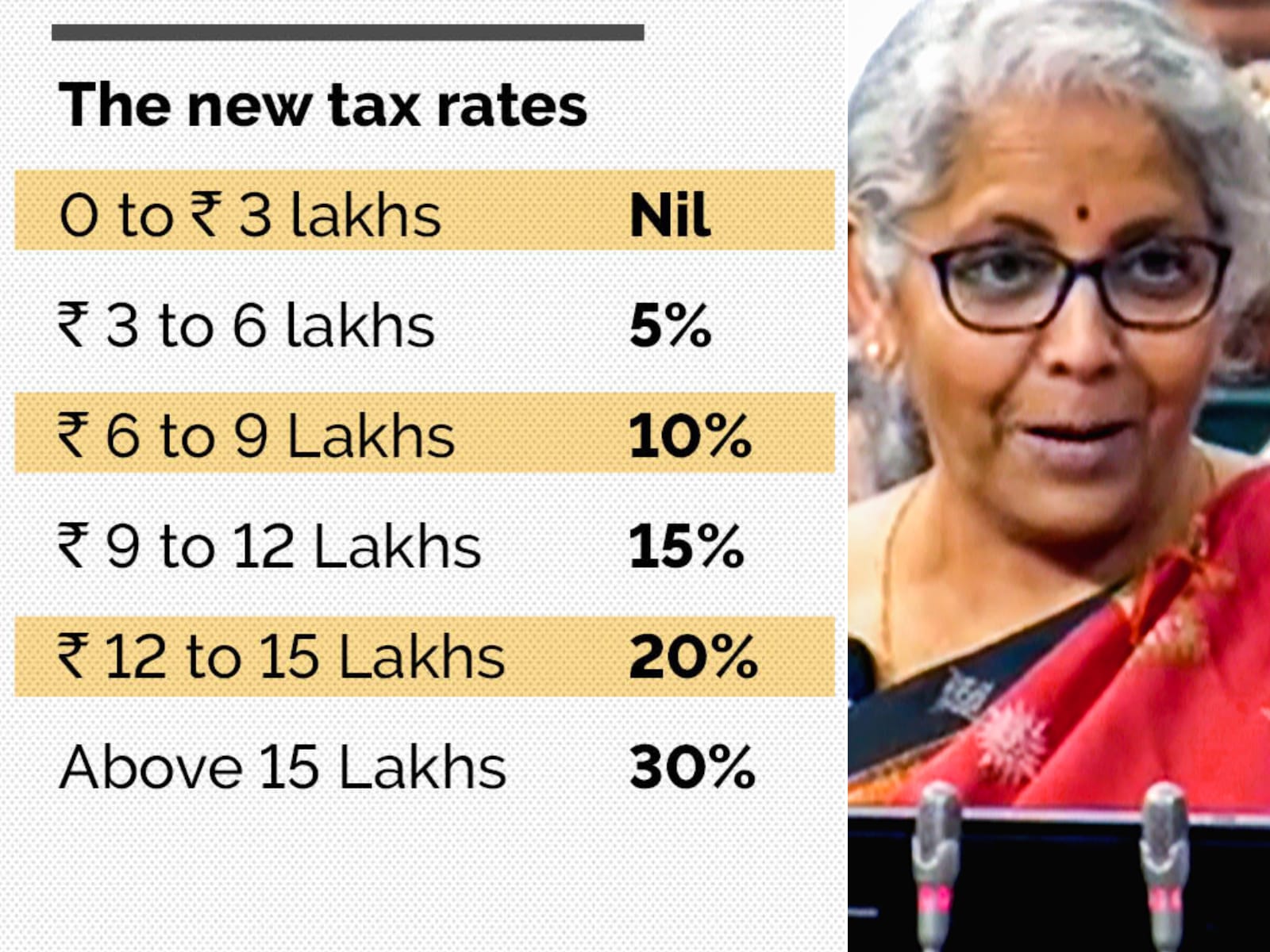

The newly introduced Finance Bill 2024 has set the stage for significant tax changes in India, particularly for salaried employees and property buyers. Starting from October 1, 2024, the amendments will allow tax deductions at source on salary income to consider various other income streams and taxes collected at source (TCS).

Under Section 192 of the Income Tax Act, it was previously stipulated that while calculating Tax Deducted at Source (TDS) on salary income, only other sources of income were to be taken into account without the allowance for TCS. This meant that employees often had to wait until filing their returns to reclaim their TCS, locking up potential funds.

With the new amendment, however, any TCS paid, alongside any TDS already deducted under other sections, can now be taken into account when calculating TDS on salary. This change is seen as a significant relief, as it will help provide more liquidity to salaried employees. No longer will they face the dilemma of a deferred refund; rather, they can benefit from adjustments right at their source of income.

This shift is not just a small tweak; it’s a game changer for anyone on a salary. Imagine having a little extra cash flow because your deductions are being calculated more accurately from the outset. It’s expected to have a positive impact on day-to-day financial planning for many employees across the country.

In addition to the adjustments for salaried workers, the Finance Bill has also clarified provisions related to the sale of immovable properties. As outlined in Section 194-IA, buyers of real estate are required to deduct 1% of the sale value as TDS if the payment or stamp duty value exceeds ₹50 lakh. However, there was confusion in instances where multiple buyers or sellers were involved.

The Finance Bill now clarifies that even when no single buyer or seller pays or receives more than ₹50 lakh, the aggregate amounts paid will be considered. This ensures that revenue isn’t missed out on due to previous ambiguities, providing a clearer path for compliance with tax laws.

The amendments will also affect renters. Currently, under Section 194-IB, individuals or Hindu Undivided Families (HUFs) paying rent exceeding ₹50,000 a month need to deduct TDS at a rate of 5%. However, with the new Finance Bill, this TDS rate will be halved to just 2%, again easing the financial burden on tenants and creating a more manageable rental environment.

Another notable change pertains to the tax collected in the name of minors. Previously, any TCS collected on behalf of minors could only be utilized against the tax liability of the minor themselves. This led to complications when the income of the minor was clubbed with a parent, causing issues in overall tax planning.

Under the new provisions, parents will be able to adjust TCS credits in the name of a minor against their own tax liabilities, simplifying tax filings. However, this adjustment will only apply when the minor’s income is clubbed with that of the parent. If a minor’s income is nil, it’s still unclear how this provision will function, leaving room for further clarification from the Central Board of Direct Taxes (CBDT).

Furthermore, the Finance Bill introduces new provisions for tax deductions relating to payments made to partners in a partnership firm. Under the proposed Section 194T, any partnership firm making payments over ₹20,000 to its partners in a financial year will now be required to deduct TDS at a rate of 10%. This is a move to bring more transparency and compliance to payments made within partnerships.

The timeline for these amendments is critical. While the changes that affect TDS on salary and property purchases will kick in on October 1, 2024, the new provisions concerning payments to partners will come into effect starting April 1, 2025. Taxpayers will need to prepare for these shifts as they navigate the updated tax landscape.

Overall, the Finance Bill 2024 seeks to ease the tax burden on various segments of the population while ensuring compliance and revenue retention for the government. As individuals and businesses alike prepare for these changes, the hope is that these measures will foster a more equitable and efficient tax system in India.