Business

Bank of England Cuts Interest Rates: What It Means for Homeowners

LONDON, England — The Bank of England lowered interest rates from 4.5% to 4.25% during its May meeting, marking the second reduction in 2025. Analysts anticipate additional cuts later this year as the central bank aims to control inflation.

Interest rates play a crucial role in the UK economy as they determine borrowing costs for mortgages, credit cards, and savings. The base rate set by the Bank indicates how much banks pay to borrow funds, which in turn affects what they charge consumers for loans and pay on savings.

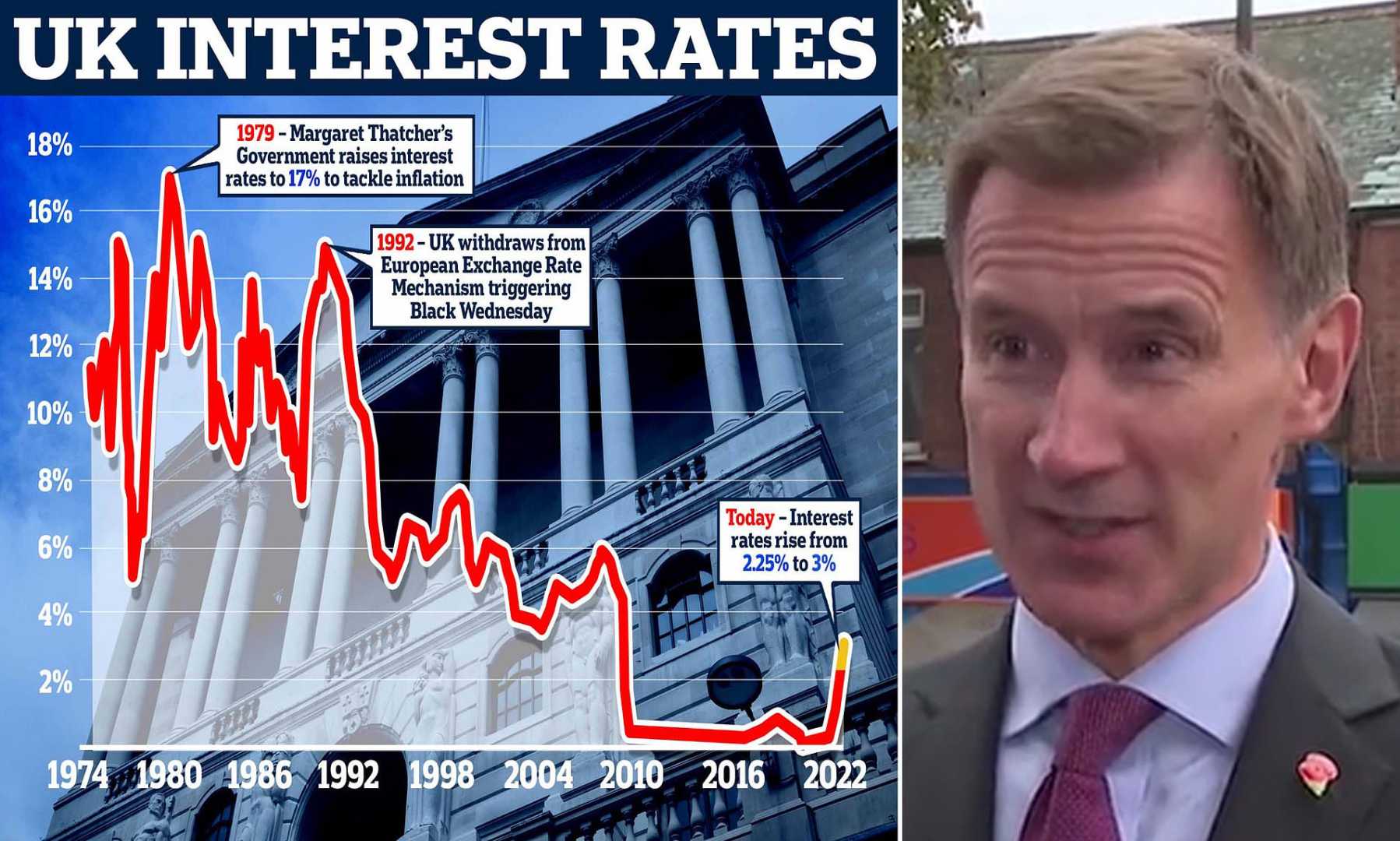

Currently, UK inflation stands above the target of 2%, despite a slight decline in the Consumer Price Index (CPI) from last month. The peak was recorded at 11.1% in October 2022. Higher inflation often prompts the Bank to raise interest rates to curb spending. Conversely, when inflation nears its target, the Bank may lower rates to stimulate growth.

Recent challenges, including the ongoing impact of US tariffs, affect the Bank’s decision-making process regarding interest rates. Andrew Bailey, governor of the Bank of England, indicated a cautious approach to reducing rates. However, evolving economic conditions may lead to deeper cuts than anticipated, with some experts suggesting rates could drop to 3.5%.

About one-third of UK households have a mortgage, with approximately 600,000 homeowners on tracker mortgages. For these borrowers, the recent base rate reduction equates to monthly savings of about £29. However, most mortgage customers are on fixed-rate deals, which buffer them from immediate rate changes but affect future lending costs.

As of May 8, the average two-year fixed mortgage rate reached 5.14%, while a five-year deal was at 5.08%. Many borrowers are facing significant costs compared to previous years, as approximately 800,000 fixed-rate mortgages at or below 3% are expected to expire annually until 2027.

In addition to mortgages, the Bank’s base rate influences credit cards and personal loans. If the Bank reduces rates, lenders may lower their interest charges over time. However, this process is usually gradual.

Savers could be adversely affected by the falling base rates, as returns on savings accounts may decrease. Currently, average interest rates offered for easy access accounts stand at about 3% annually. Savers reliant on interest income may face financial challenges due to these reductions.

The broader economic landscape in the UK correlates closely with international markets, particularly influenced by changes in the US Federal Reserve‘s policies. The Fed recently maintained interest rates within a target range of 4.25% to 4.5% despite raising them three times in late 2024.

Future mortgage rates will depend largely on forthcoming economic reports and market forecasts. As expectations point towards more favorable rates, homeowners and potential buyers are advised to stay informed and act accordingly.