Business

Analysts Split on Palantir’s Future Amid AI Market Volatility

NEW YORK, NY — Investors are grappling with diverging opinions on Palantir Technologies as the artificial intelligence market remains volatile. Since the start of 2023, AI has rapidly transformed investor sentiment, with predictions suggesting it could enhance global GDP by up to 26% by 2030, according to reports by PwC. As Palantir’s stock fluctuates dramatically, analysts are divided on the company’s prospects.

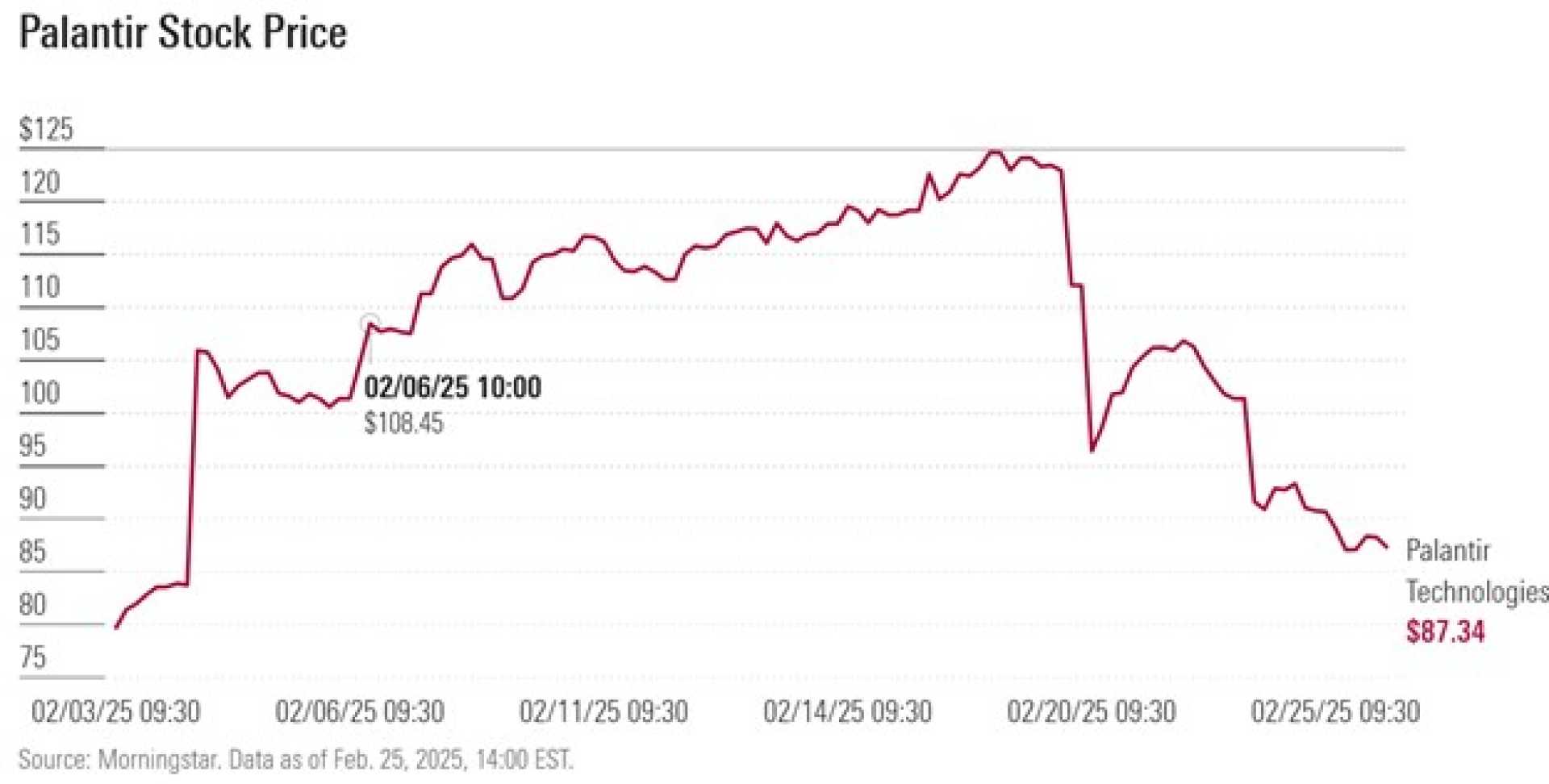

Palantir Technologies, once considered a frontrunner alongside Nvidia in the AI landscape, presented a nearly 2,000% gain in its stock over the past two years, reaching a peak price of $85.85. However, analysts now project that its shares could either soar by 46% or plummet by 53% depending on market conditions.

Mark Schappel of Loop Capital Markets is one of the company’s staunchest advocates, maintaining a buy rating and setting a price target of $125 per share. He stated, “Palantir’s unique positioning with its Gotham and Foundry platforms allows it to generate predictable sales and cash flow, which is crucial for long-term growth.” Schappel believes that the company’s multiyear contracts with U.S. government agencies provide stability and transparency in cash flows.

Gotham, which assists federal governments in data collection and military planning, has been a consistent revenue driver for Palantir. In contrast, the Foundry platform is gaining momentum, adding 571 commercial customers in 2024 alone — a 52% increase from the previous year. Schappel emphasizes, “Foundry is just at the beginning of its growth potential and is essential for businesses looking to leverage data for efficiency gains.”

On the other hand, Rishi Jaluria of RBC Capital Markets holds an underperform rating, suggesting that Palantir’s stock may drop to $40. He argues that this drop would reflect a downside of 53% from where shares were last priced. Jaluria’s skepticism stems from concerns over Palantir’s lofty valuation, especially as the company’s price-to-sales ratio soared around 100 at its peak.

“Palantir’s high valuation is unsustainable given historical trends in the tech industry. No company has maintained such multiples without facing significant corrections,” Jaluria stated. His analysis is further supported by predicted cuts to the U.S. defense budget, which may impact Palantir’s core business dealings.

The U.S. Pentagon is expected to reduce its budget by approximately $50 billion annually over the next five years. Analysts fear these cuts could limit the number of new defense contracts available to Palantir, which has heavily relied on its government dealings for growth. Jaluria added, “The long-term ceiling for Palantir’s Gotham platform may be constrained due to its limited client base, primarily the U.S. and its allies.”

Despite the emerging fears, Palantir’s subscription-based Foundry platform demonstrates significant growth potential. If the AI market faces a downturn, Palantir might still maintain stable sales due to its contract structures. However, if the market sentiment remains unfavorable, high valuation stocks like Palantir could face increased downward pressure.

Historically, transformative technologies often face overhyped valuations leading to eventual corrections. Investors have routinely overestimated adoption rates of new advancements, and Palantir’s current valuation may be one of the latest examples. “The historical data clearly indicates that stocks with extreme price multiples often experience declines after periods of exuberance,” noted investment expert Charles Brown.

In conclusion, as the market for AI technologies continues to evolve, so too will the strategies and valuations for companies like Palantir. The divergent opinions among analysts highlight a critical turning point for investors as they navigate the complexities of the burgeoning AI landscape.