Business

Insurers Drop Key Car Insurance Clause, Leaving Consumers Vulnerable

LOS ANGELES, California — A key consumer protection in car insurance policies is disappearing, leaving drivers at risk of bearing higher repair costs after accidents. The right to appraisal (RTA), which allows policyholders to request a third-party review when disputes arise about repair costs, is being quietly removed from some auto policies.

Repair professionals are sounding the alarm as insurance companies increasingly push back against legislation that mandates the inclusion of the appraisal clause. In May 2025, two states passed bills to uphold this consumer right, but many areas remain unprotected.

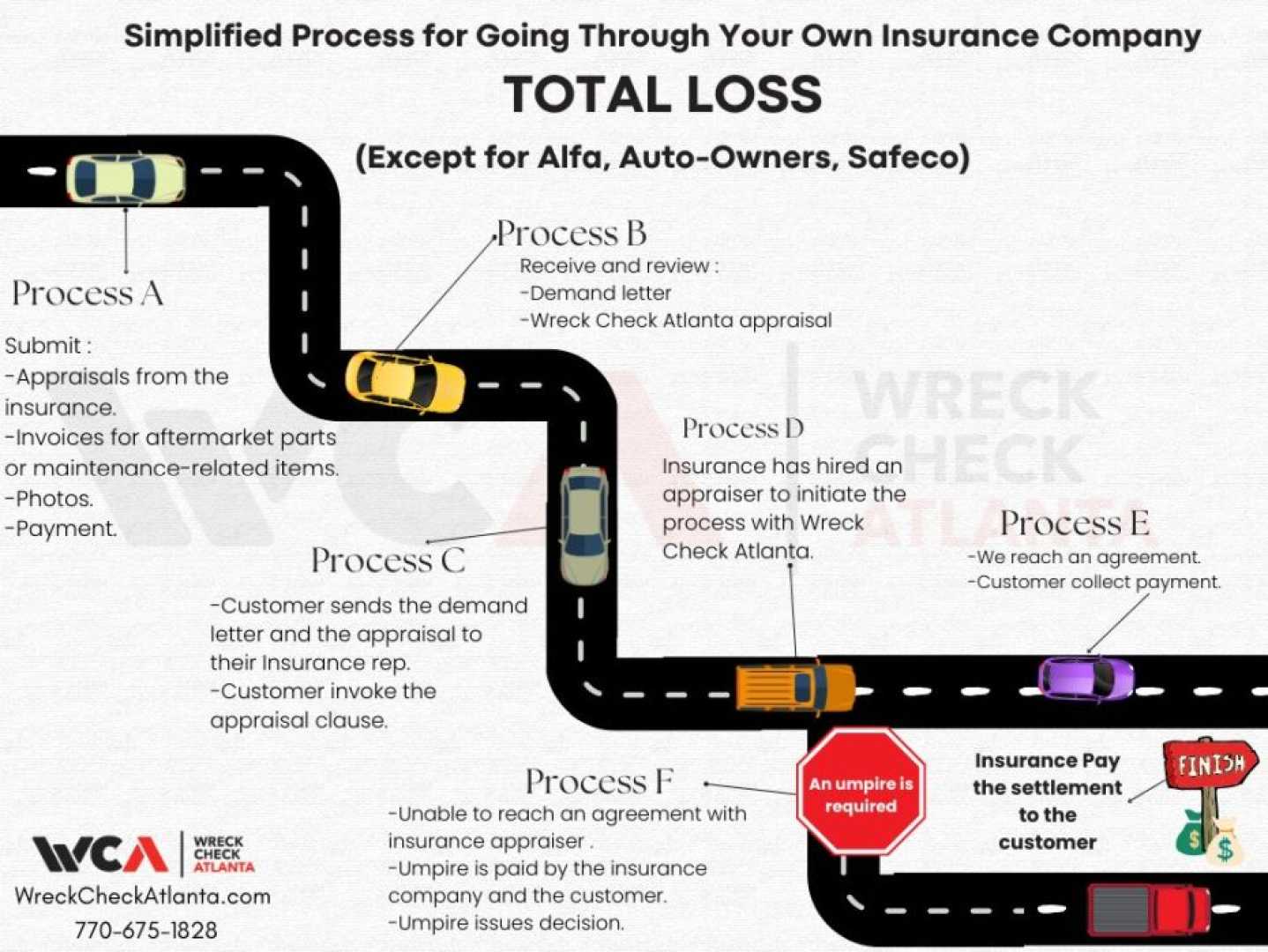

“Disagreements are going to happen,” says Andrew Batenhorst, a body shop manager in California. “There should be mechanisms in the policy that allow for an independent party to mediate these types of situations.” When insurers and repair shops can’t agree on costs, consumers can utilize the RTA to avoid hefty out-of-pocket expenses.

Batenhorst reports that invoking the right often leads insurance companies to pay fairly for the damages. However, he warns that the insurance industry has not embraced this clause. Insurance companies view the appraisal process as a potential burden, contributing to rising operational costs.

Brandon Vick, a regional vice president at the National Association of Mutual Insurance Companies, acknowledges that while appraisal clauses are standard, there are concerns that requiring them could increase fees for consumers. “We believe generally that these are private contracts, and any additional mandate will likely carry some sort of cost,” he states.

In states like Washington, where Senate Bill 5721 aims to enforce the right to appraisal, concerns are mounting among insurers about the financial implications. Opponents argue that such laws will slow down the repair process, leading to even higher claims costs over time.

Despite these concerns, Rhode Island serves as a case study. After establishing a right to appraisal law in 2023, the state saw a 20% increase in vehicle insurance premiums, but not as steep as the national rise of 31% during the same period.

For consumers unsure if their policy includes an appraisal clause, it’s crucial to review the physical damage section of their insurance documents. Familiarity with these terms can empower policyholders when disputes over repair costs arise.

As lawmakers in other states consider similar legislation, the future of the right to appraisal hangs in the balance. Until then, the removal of this consumer protection by insurance companies raises serious concerns about fairness and accountability in auto insurance.